|

Listen to this post if you prefer

|

Using senior debt for a real estate transaction is almost always a no-brainer. The question becomes: for how much loan will the property qualify? We discuss this below.

Senior debt financing for development and construction of a new property

A real estate development project will quality for as much in terms of % of total development cost (excluding financing costs) as the senior lender is willing to wager it could safely get back in a liquidation of the completed property. In other words, lenders are in the business of loaning money and getting it back, and in addition, earning interest on that principal amount they lend. In the case of a borrower default, the lender has the right to foreclose on the property. But then what? Lenders are not developers… they don’t want to be in the developer’s seat. So if they do in fact foreclose, they will oversee the completion of the project and liquidate it (sell it quickly) to recoup the principal outstanding on their loan, which includes accrued interest.

For most senior construction lenders, their maximum willing exposure tops out around 65% of loan to cost (LTC). This loan ceiling is imposed and upheld by the bank’s credit committee.

Senior debt financing for existing income-producing properties

Things are a little different for cash flowing properties. There are three main tests used to “size” a senior mortgage loan:

- Loan to value test

- Debt service coverage ratio test

- Debt yield test

Let’s go through them one by one.

The Loan to Value (LTV) test

This test is based on the value of the property related to its adjusted NOI (net operating income after reserves). The lender will apply a cap rate to the trailing 12 month’s worth of adjusted NOI, deriving a property value. Assuming the property will successfully appraise to this value, the lender will then apply their (credit committee-given) maximum Loan to Value percentage (e.g., 70%) to size the loan. Here’s an example with round numbers:

Trailing adjusted NOI: $500,000

Cap rate: 8.00%

Gross valuation: $500,000/.08 = $6,250,000

70% Loan to Value = $4,375,000

The debt service coverage ratio (DSCR) test

This test sizes the loan based on the minimum required debt service coverage ratio based on the lender’s internal requirements. The DSCR is the number of times that the property’s adjusted NOI must “cover” the annual debt service (both principal and interest payments combined). Lenders want to have sufficient cushion from the property’s cash flows such that should the property lose some portion of its tenants, the cash flows from the remaining tenants will still be enough to service the debt in full each month.

DSC ratios for real estate are typically between 1.20x and 1.50x, with higher coverage ratios applying to riskier cash flow streams.

To continue the example from above:

Trailing adjusted NOI: $500,000

Lender minimum DSCR: 1.20x (Therefore, annual loan payment that could be supported: $500,000/1.2 = $416,666.67)

Loan size, back-solved for using the Present Value (PV) function: =-PV(rate, nper, pmt)

Since payments are made monthly, we divide the annual rate by 12, and multiply the years of amortization by 12 to solve for the present value of the loan that results in the monthly payment of $416,666.67/12. Assuming the rate is 5.00% and the term of amortization is 30 years, the function is populated in Excel as =-PV(.05/12,30*12,$416,666,67/12), with the result being a loan amount of $6,468,111.17

Debt yield

Debt yield is calculated as the property’s adjusted NOI divided by the loan principal amount. Some people refer to this as the “lender’s cap rate”. Lenders will underwrite to a yield they feel is acceptable given the risk of the cash flows coming from the property. A 10%+ debt yield as a minimum is a common rule of thumb .

Generally speaking, the lender will choose the lower of the two loan sizes generated by the first two tests, and then ensure that the debt yield is satisfactory. So if the lender selected the $4.375MM loan amount, the debt yield would be $500,000 / $4.375MM, or 11.42%.

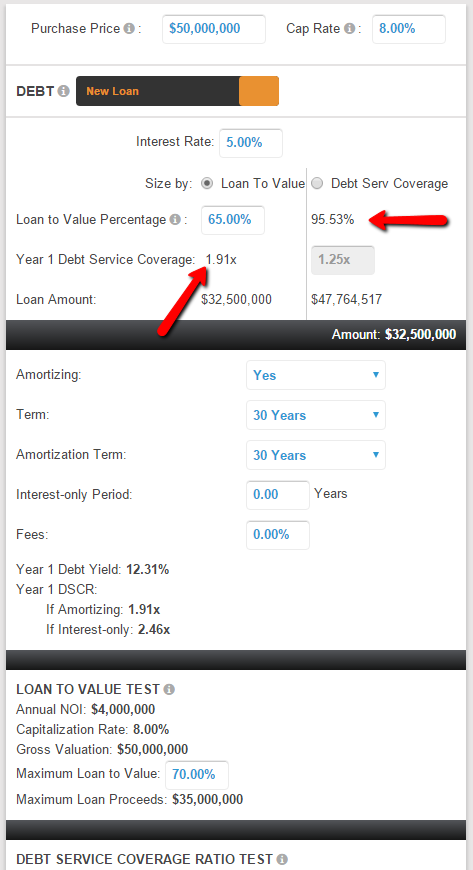

How Valuate makes this all very easy

When it comes to sizing senior acquisition loans, Valuate does all of the hard work for you. The neat thing about how Valuate presents loan sizing is that it persistently displays the loan amounts and DSCRs for both test methods so you can always see what the alternative to the method chosen would yield.

or

Please post questions below.