There is something of a mystery surrounding the mechanics of Senior Construction Loans. Here’s our plain-English attempt to provide better clarity:

1. The Senior Construction Loan is not drawn down in a lump sum at Time 0 as is the case with an Acquisition loan for an existing income-producing property. Rather, it is drawn down from the Lender monthly in amounts to match costs incurred over the prior month. The rationale behind the Borrower making piecemeal monthly draws is to incur interest costs on only those funds that they have had a need to draw down. The rationale for the Lender is to only disburse funds for which there is existing collateral (e.g., land purchased, construction work put in place to date) upon which a lien can be placed.

The other main distinction between a construction loan and an acquisition loan is that Construction Loan Interest will accumulate rather than be paid current each month. This is often referred to as having interest that “accrues” or is “capitalized” (tracked cumulatively in addition to the cumulative funds actually disbursed to the Borrower, and charged against the total loan size; see point 3 below). The rationale for the Borrower not having to pay interest current is that the asset that would generate the funds to pay the debt service does not yet exist.

2. Some development costs are not eligible for Senior Loan funding (e.g., Loan fees for a Mezzanine loan). The Senior Lender will only lend against items that have some potential liquidation value to them in the instance of a foreclosure. If a Senior Lender has to foreclose on a development project, they have no claim to the origination costs paid to another Lender, thus there is no collateral value that can be liquidated.

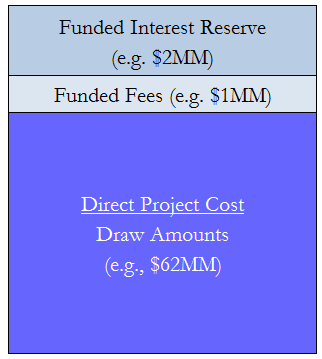

3. The Senior Loan Principal Amount (the loan size) is comprised of:

- Dollar amounts that will be used to fund eligible land, hard and soft costs (“Direct Project Costs”)

- Dollar amounts that will be set aside for Interest that is generated by the Senior Loan but not paid current (“Funded Interest Reserve”)

- Dollar amounts that will be set aside for Senior Loan Fees that are generated but not paid current (“Funded Fees”)

In other words, the Borrower does not have access to the entire nominal Loan Amount for funding of Direct Project Costs. This is because ALL dollar amounts, whether funded towards Direct Project Costs, or set aside, represent financial exposure of the lender (i.e., their Loan-To-Cost %, or “LTC”) to this development project. See the example below.

Illustrative “Uses of Funds” of a $65MM Senior Construction Loan

4. Once the Senior Lender’s total financial exposure to the project equals the $65MM Loan Principal Amount, the funding and setting aside of dollar amounts will cease, and the Borrower will likely need to make cash interest payments from that point forward

5. The entire $65MM Loan Principal Amount is repaid to the Lender through asset sale net proceeds, or through a refinancing with a Permanent Loan.