This is the first in a series of posts regarding the most widely used and least understood real estate investment performance metric, the Internal Rate of Return, or IRR. Could life on the Internet possibly get any more exciting than this?!

Mixed-use Condominiums in Washington, DC's Logan Circle Neighborhood. Uses in addition to the luxury residential lofts include retail and a below-grade health club.

When evaluating a potential real estate investment such as the ground-up development of the mixed-use condominium building above, we often turn to the Internal Rate of Return as a measurement of transaction performance and attractiveness. However, many do not really understand what IRR is, when it is a meaningful measure, and when it is not. I will do my best to remedy this. Please forward this post on to those for whom you feel it would be helpful. Thanks!

A metric by any other name. IRR could not have a more confusing name. Does anything visual come into your mind’s eye when someone says “internal rate of return”? It’s quite possibly the least intuitively-named measure of financial performance compared to the clarity of Multiple on Equity Invested or Return on Cost.

What it is. IRR is a cumulative measure of the performance of a cash (equity) investment made in one or more accounting periods (months, quarters or years), where the very first cash flow over the investment horizon is the initial investment made at Time Zero.

The transaction’s “performance” as reflected in the IRR percentage can be thought of as the overall result of the one or more periods of cash investments (negative cash flows) made, as evaluated on and influenced by a) the size of the individual periodic net positive cash flows that result from the investment or investments made, and b) the timing of each of these differently-sized positive cash flows in the course of the entire transaction timeline, and relative to one another.

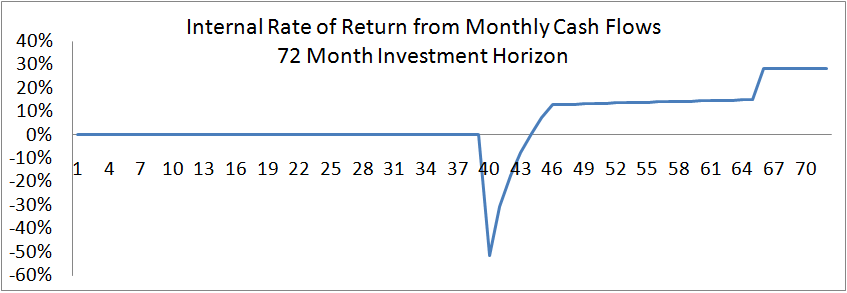

How it starts out. Ask yourself the following question: what is the performance of the initial Time Zero cash investment one millisecond after it is invested (assuming no positive cash flows are received during that millisecond): zero, or infinitely negative? To inform our answer, let’s take a look at graphs of investments, cash flows and the corresponding IRR for a residential condominium development project with ground floor retail.

Equity funds site control, soft costs, the first few periods of construction hard costs (Months 17-19), and the operating deficit (Months 34-36). The construction loan funds the balance of construction hard costs, as well as its own interest payments. The Month 48 spike in Equity Net Cash Flow after the residential unit closings end shows how impactful the sale of the retail condominium units are to the project's profitability and Internal Rate of Return.

As seen in the bottom two graphs, the IRR does not go positive until after all equity has been recouped and our Cumulative Net Equity Cash Flow is zero at Month 44.

The Takeaway. What is important to understand is that the IRR starts out negative — really negative. We note that Excel cannot calculate an infinitely negative value, thus a numeric value for the IRR in the bottom graph does not appear until it is only “slightly” negative at around -50% at Month 40. The lesson to take away from this is that for the IRR to become positive, ALL invested capital must first be returned. But that only gets you to a 0% IRR. To get a positive IRR, you need to continue to net cash after you receive all invested capital back, i.e., get a return ON your capital, not just a return OF your capital.

What questions about IRR can I answer for you?

{kind=link}