Mezzanine financing is a sometimes confusing part of the capital structure in a real estate transaction. Part of the reason for this is that the term mezzanine is really a catch-all for an entire category of non-senior mortgage debt, non-common equity instruments that can fill a capitalization gap between them.

Mezzanine (“middle”) financing can take the form of debt or equity, more specifically:

- Junior debt, such as a second mortgage

- Preferred equity

- Convertible debt

- Participating debt

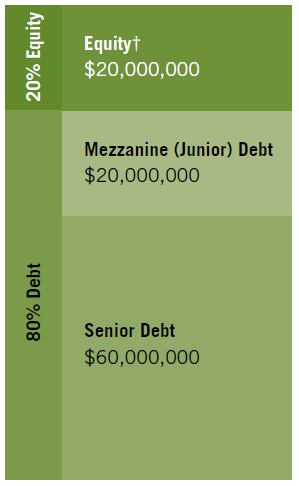

Senior mortgage debt is legally secured, or collateralized, by the physical property and the associated cash flows. A lien is placed on the property and recorded with the government to certify this legal relationship.

In all cases, the mezzanine instrument is subordinate to the senior debt, and in virtually all cases, the mezzanine instrument is not secured by the property, but rather by the equity in the entity that owns the equity in the property. As such, the mezzanine position is a riskier one to be in, and for this reason, the cost of mezzanine capital is higher than that of senior mortgage debt.

Assuming the mezzanine takes the form of junior debt, it would be modeled as follows:

- for developments, the mezzanine will fund before the senior construction loan, and it will be repaid only after the senior loan is repaid in full. Your sources of funds formulas will need to reflect this priority of funding and lack of priority of return of principal.

- for acquisitions, assuming all loans fund simultaneously at closing, there is nothing to do with respect to priority, but the repayment of the mezzanine loan needs to be on a residual basis to the repayment of the senior loan.

If the mezzanine financing takes the form of preferred equity, the funding will depend on the joint venture operating agreement between the mezzanine investor and the property equity sponsor. The preferred shares will give the holders of those shares some set of specified rights above that of the common equity, but again, it will still be subordinate to the senior debt. An example is that the preferred equity will participate in a priority preferred return whereas the common equity will not.

Convertible debt provides the debt with the option to convert into common equity at specific terms, and participating debt will receive interest payments and also participate in income above a specified level.

Our Professional versions of our Excel model templates include an interest-only mezzanine loan as part of the capital stack.

Interested to know more about mezzanine financing? Check out this post for things to consider related to taking on mezzanine debt and this audio interview for details on inter-creditor agreements between mezz and senior lenders.

Pretty good description. Also would mention the strict Intercreditor Agreements to which the mezz lender would be party with the counterparty senior lender on cure and standstill rights, that could significantly impact the mezz lender’s position. Further, the mezz position is also inherently riskier on the basis that a default on the senior debt would not constitute a default on the mezz, thus providing for more rights conveyed the senior lender on foreclosing on the assets to protect its position and further place the mezz debt at risk from principal recovery.

Thanks Vostok, great additions! We talk more about mezz in this audio interview for folks who have not listened to it yet https://www.getrefm.com/blog/financing/mezzanine-financing-and-intercreditor-agreements-explained-dr-peter-linneman/

an equal discussion about mezzanine loans for real estate can also be found at http://www.commercialproperty-financing.com/mezzanine-loan/. Mezzanine loans are good for Acquisition, Recapitalization, Construction, and Refinancing