|

Listen to this post if you prefer

|

We’ve written on what is a good IRR for a real estate transaction, and in that post we touched briefly upon the equity multiple. Here we will expand on it.

What is the multiple on equity?

First, a definition. The multiple on equity (aka equity multiple, multiple on invested capital, return on equity) is simply the number of times that the total equity investment is returned. Put another way, how many times you (as the equity) got your money back.

A mentor of mine used to say that equity multiple is chunk dollars, “dollars you can eat,” whereas you can’t eat IRR.

The formula for equity multiple is: (net cash flow to equity/total equity invested) + 1

Note that the total equity invested should be represented as a positive value.

The reason for the +1 in the equation is due to the numerator being net, not gross, cash flow. Net means that the investment amount was characterized as a negative amount (a cash outflow), which reduces the positive cash flows by its nominal amount. Adding the 1 back allows the equity multiple to get credit for the return of the investment amount in full.

An example multiple on equity calculation

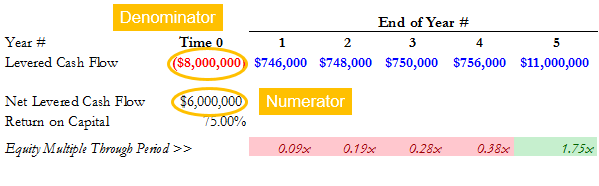

As seen below, if the investment amount is $8MM, and the cash flows over the 5-year holding period are as shown, the net cash flow = $6MM (positive cash flows = $14MM). The Net Levered Cash Flow of $6MM represents a return of the $8MM invested, and profit on top of that of $6MM, for an equity multiple of 1.75x.

As you can see, the equity multiple remains below 1.00x until the last of the $8MM in invested capital is returned, which occurs in year 5. It’s also in year 5 that the $6MM of profit is earned, driving the multiple above 1.00x to 1.75x.

What equity multiple is typically targeted by investors? Is there any data on this?

Have you ever met anyone who didn’t want to double their money? Neither have I. But what we want and what is a reasonable expectation often do not match up. One consideration that investors keep in mind is the amount of time that the investment is in play. You would be laughed at if you thought you could double your money in real estate in 1 week because you can’t even complete due diligence and go to closing in that short amount of time, let alone flip the property as well. An extreme example, yes, but it illustrates that at a minimum, investor returns are governed by the realities of the pace of the business.

The 1-week double your money scenario reminds us that while the math that computes the IRR does take into account the passage of time, the equity multiple ignores the passage of time altogether. If it were possible to double your money in a week, your IRR would be so high (above 1,000%) that it’s clownish.

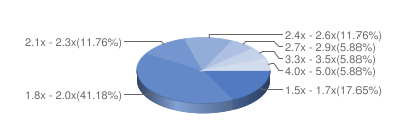

Nevertheless, generally speaking, a 2.00x deal-level multiple is sought, with targets below that for less risky, shorter-term deals (acquisition of a core stabilized property), and targets above that for more risky, longer-term deals (development in an up and coming submarket). See the pie chart of REFM’s survey below.

The data in the pie chart is gathered on a continual basis in our CRE JV Equity Partnership Structure Database.

Remember, though, sponsors and investors often have a promote structure built in, so there will actually be three equity multiples: deal-level, sponsor, and investor. You can learn more about promotes and get Certified on this topic in our Level 3 Bootcamp.